| Want to send this page or a link to a friend? Click on mail at the top of this window. |

| More Books and Artsl |

| Posted December 28, 2008 |

| DEBT SWEAT | |

| Printing Money - and Its Price | |

|

|

|

|

|

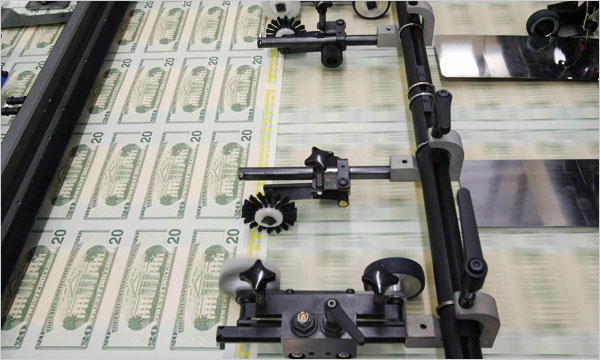

| JIM YOUNG/REUTERS | |

|

|

| By PETER S. GOODMAN |

|

|

|

|

|

| CHIP LITHERLAND FOR THE NEW YORK TIMES | |

|

|

| Wehaitians.com, the scholarly journal of democracy and human rights |

| More from wehaitians.com |