| Want to send this page or a link to a friend? Click on mail at the top of this window. |

| More Books and Arts |

| Posted July 20, 2008 |

|

|

|

| THE NATION | |

| Too Big to Fail? | |

|

|

|

|

|

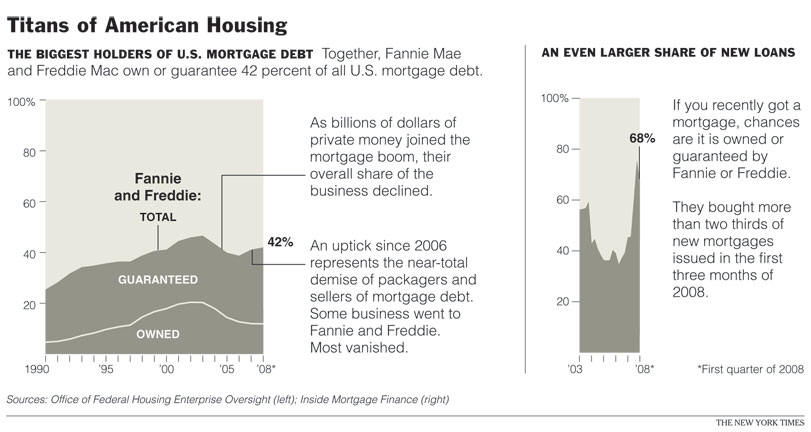

| PETER AND MARIA HOEY | |

|

|

| By PETER S. GOODMAN |

|

|

| JOSHUA ROBERTS/BLOOMBERG NEWS |

| Christopher Cox, the S.E.C. Chairman, left, and Ben Bernanke, the Fed chairman, center, hear Treasury Secretary Henry Paulson tell senators he wants authority to help save Fannie Mae and Freddie Mac. |

| Wehaitians.com, the scholarly journal of democracy and human rights |

| More from wehaitians.com |