| Want to send this page or a link to a friend? Click on mail at the top of this window. |

| More Books and Arts |

| Posted August 23, 2010 |

| Income Inequality and Financial Crisis |

|

By LOUISE STORY |

|

|

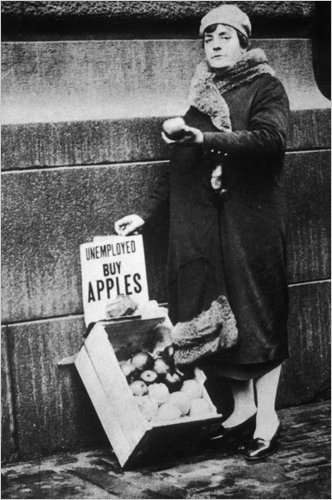

HULTON ARCHIVE/GETTY IMAGES |

| SCRAPING BY in depression era New York City, scenes like this underscored the sudden hardship. |

| Wehaitians.com, the scholarly journal of democracy and human rights |

| More from wehaitians.com |