| Want to send this page or a link to a friend? Click on mail at the top of this window. |

More Special Reports |

| Posted August 21, 2009 |

| National |

| After 30-Year Run, Rise of the |

| Super-Rich Hits a Sobering Wall |

|

|

PHOTOGRAPHS BY CHRIS RICHARDS FOR THE NEW YORK TIMES |

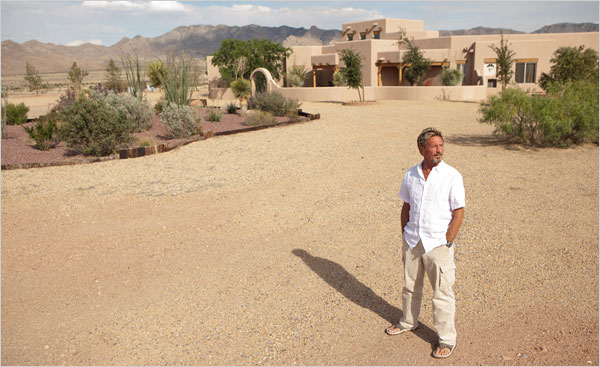

| John McAfee is auctioning off this property in New Mexico to pay bills. His worth has fallen to about $4 million from a peak of about $100 million, |

|

By DAVID LEONHARDT |

|

and GERALDINE FABRIKANT |

| No More '50s and '60s |

|

|

|

|

|

| Mr. McAfee, who made his fortune in antivirus software, bought the property to have a place to fly-open-cockpit planes with his friends. | |

|

|

| Making More Money |

|

|

|

|

|

|

|

| Stock Market Mystery |

| Wehaitians.com, the scholarly journal of democracy and human rights |

| More from wehaitians.com |